Sign in

Sign in

Let’s be real: getting declined for payment processing stings.

You’ve built a business. You have customers ready to pay. And then some underwriter you’ve never met decides to pump the brakes — often without a clear explanation. It feels arbitrary. It feels personal. And if you don’t know why it happened, it’s hard to know what to do next.

Here’s the good news: most declines are fixable. And once you understand why they happen, you’re already halfway to getting approved.

Let’s break it down.

The Underwriter Isn’t Your Enemy

First, a mindset shift. When a processor declines your application, they’re not making a judgment about you as a person or entrepreneur. They’re running a risk calculation. Processors take on financial liability every time they board a new merchant — if you process payments and then disappear, issue a flood of chargebacks, or operate in a legally gray space, they’re on the hook.

So everything that follows comes down to one question the underwriter is trying to answer: Is this merchant a liability?

Your job is to make the answer obviously, undeniably no.

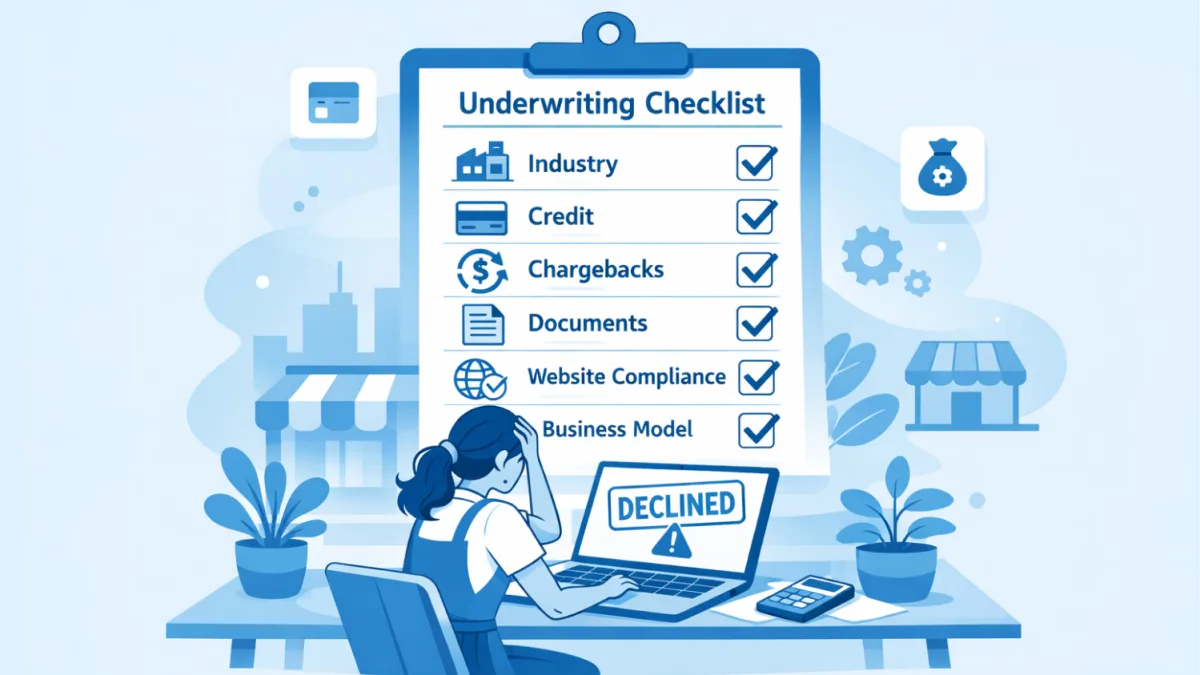

The Most Common Reasons Merchants Get Declined

1. You’re in a High-Risk Industry

Some businesses trigger automatic scrutiny — not because there’s anything wrong with them, but because their category carries a statistically higher rate of chargebacks, fraud, or regulatory complexity. Think nutraceuticals, firearms, adult content, travel, credit repair, CBD, subscription boxes, or online gaming.

If your business falls into one of these categories, standard merchant accounts may not be the right fit. That doesn’t mean you’re out of options — it means you need a processor that specializes in high-risk accounts. At Merchant Service Depot, this is exactly what we do. Getting you approved isn’t a problem to work around; it’s our core offering.

2. Bad Credit or a Troubled Financial History

Processors pull credit. Personal credit, business credit, or both. Bankruptcies, tax liens, judgments, or a pattern of financial instability raise red flags. They signal risk, and risk means potential losses for the processor.

The fix: Know your credit profile before you apply. If there are issues, address them proactively — or work with a processor that offers solutions for merchants who don’t have a perfect financial track record. Transparency goes a long way. Don’t hide problems; explain them.

3. Excessive Chargeback History

This is a big one. If you’ve had a merchant account before and your chargeback ratio was above 1%, that data follows you. The card networks (Visa, Mastercard) maintain databases — MATCH and VMSS — that flag merchants who’ve been terminated for chargeback abuse or fraud. Being on the MATCH list is one of the hardest holes to dig out of.

The fix: If your chargeback history is the issue, you need to show what’s changed. Have you implemented better fraud tools? Updated your return policy? Improved your customer service process? Document it. A strong remediation story matters. And if you’re not yet on the MATCH list, focus obsessively on keeping chargebacks under control before they become a career-ending problem.

4. Incomplete or Inconsistent Application

You’d be surprised how many declines come down to simple paperwork problems. Missing documents, mismatched business names, inconsistent addresses between your application and your bank statements — underwriters notice everything. Any inconsistency is a reason to pause or decline.

The fix: Before you submit, audit your application like an underwriter would. Make sure your:

- Business name matches your bank account, website, and state registration

- Processing volume estimates are realistic and backed up by financial history

- Website is live, professional, and compliant (more on that next)

- All requested documents are included and current

5. Website and Compliance Issues

Your website is part of your application. Underwriters visit it. If it’s incomplete, unprofessional, or missing required disclosures, that’s a problem. For certain industries, specific compliance elements — like clear refund policies, terms and conditions, and accurate product descriptions — are non-negotiable.

The fix: Before you apply, make sure your site is buttoned up. It should look like the website of a legitimate, established business. Include your contact information, a clear refund/return policy, terms of service, and privacy policy. If you’re in a regulated industry, make sure your disclosures are front and center.

6. Business Model Confusion

If the underwriter can’t quickly understand what you sell, how you sell it, and to whom, that’s a problem. Vague or overly complex business models — especially in e-commerce, SaaS, or marketplaces — can trigger a decline simply because the risk can’t be assessed clearly.

The fix: Be crystal clear in your application. Describe your business like you’re explaining it to a smart 10-year-old. If your model is complex, walk through it step by step and be transparent about your refund and fulfillment timelines.

What to Do After a Declin

Getting declined isn’t the end of the road. Here’s how to respond:

Step 1: Find out why. Ask the processor directly. Not all of them will tell you, but many will. You can’t fix what you don’t understand.

Step 2: Fix what you can control. Credit issues, website gaps, missing documents, chargeback patterns — most of these are addressable. Do the work.

Step 3: Apply with the right processor. If you were applying through a generic, one-size-fits-all processor, that might be your real problem. Some businesses simply need a specialist.

You Need a Processor Who Knows How to Say Yes

At Merchant Service Depot, we’ve worked with thousands of merchants — from brand-new startups to established businesses with complicated histories. We know how underwriting works because we’ve been doing this for years. And we know how to position your business for approval, not just push paperwork.

If you’ve been declined — or if you’re worried about getting declined — reach out. Tell us your situation honestly. We’ll tell you what we can do, and we won’t waste your time.

Getting approved isn’t about luck. It’s about knowing the game and playing it well. Let’s get you back to accepting payments.

Ready to get approved? Contact Merchant Service Depot today and let’s figure out the right solution for your business.

Ready to boost your payment solution

Related posts:

- Merchant’s Field Guide: Best and Worst Days to Sell Payments Solutions

- Smileyface Dollarsign: A simple introduction to happy payments.

- Top 10 Things Tech Integrators Wish They Knew Before Payments Integration: A Super Agenda and Meeting Prep Guide

- Building Million-Dollar Merchant Services Partnerships.